TYLER DURDEN …

TUESDAY, DEC 06, 2022 – 05:08 AM …

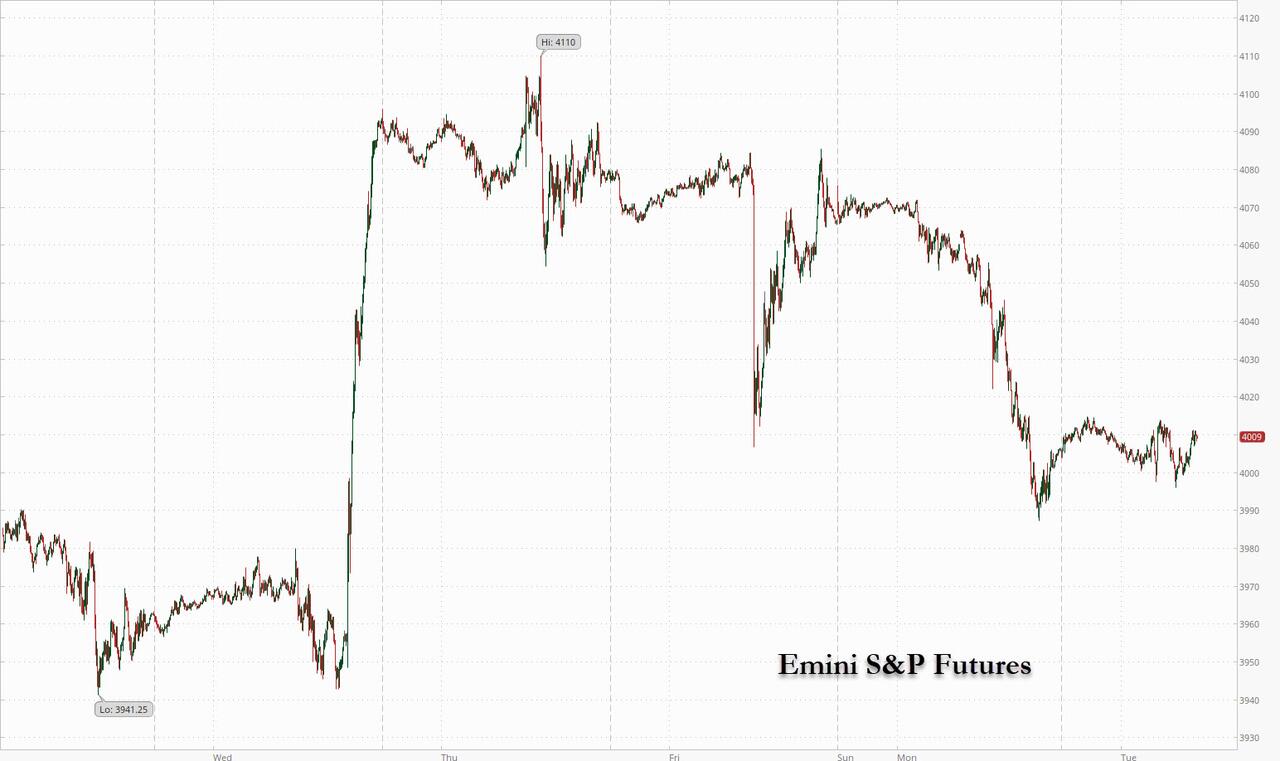

US futures trade in a narrow range on Tuesday following Monday’s rout, as investors weighed stronger-than-expected economic data and the potential that Federal Reserve rates will peak at a higher level. Contracts on the S&P 500 and the Nasdaq 100 were both up around 0.1% at 7:30am ET after trading on either side of the unchanged line earlier, signaling moderate gains for Wall Street after both underlying indexes closed lower on Tuesday, with hot US ISM services data fueling bets on a terminal Fed rate of close to 5% next year. The dollar weakened and Treasuries gained while bitcoin was unchanged.

{kind=link}

In premarket trading, Gitlab shares jumped after the software company raised its full-year revenue forecast, while JPMorgan Chase &gained slightly after losing its only sell-rating. Meanwhile, traders will have eyes on Apple as wait times for the company’s most expensive smartphones improved this week, indicating that supply chain disruptions are easing. The US Army on Monday awarded Bell Textron Inc. a contract worth up to $1.3 billion, beating out a Lockheed Martin Corp.-Boeing Co. team to replace the iconic Black Hawk helicopters by 2030. Here are all the notable premarket movers:

- Alcoa (AA) shares rise almost 0.7% in premarket trading after Bloomberg reported that the US and European Union are weighing climate-based tariffs on Chinese steel and aluminum, citing people familiar with the matter.

- General Electric (GE) rises 1.6% after it was upgraded to outperform at Oppenheimer, which highlighted the strength of the industrial and financial company’s aviation business.

- Gitlab (GTLB) shares rallied 18% in premarket trading after the software company raised its full- year revenue forecast and reported third-quarter revenue that beat expectations. Analysts said they were positive about the company’s resilience and ability to grow despite economic uncertainty and widespread IT budget cuts.

- MEI Pharma (MEIP) shares plummet 39% in premarket trading after the company and Kyowa Kirin said they’re discontinuing development of the experimental cancer drug zandelisib outside of Japan, citing guidance from US regulators. Truist Securities and BTIG downgrade MEI, while Stifel places estimates for the company under review.

- Mirati Therapeutics, Inc. (MRTX) slides 14% in premarket trading after the company shared data from a study of its adagrasib therapy in combination with pembrolizumab (Keytruda) for patients with an advanced form of lung cancer, resulting in an objective response rate of 49%.

- NRG Energy Inc. (NRG) agreed to buy Vivint Smart Home Inc. for $2.8 billion in an all-cash deal, accelerating its consumer-focused growth strategy. Shares decline 8.2%.

- Sumo Logic (SUMO) shares jump 9.5% in US premarket trading after the analytics-platform provider boosted its revenue guidance despite a tough macroeconomic backdrop, with analysts particularly positive on the firm’s intention to shorten its path to profitability.

- Vivint Smart Home (VVNT) jump 32% in premarket trading after NRG Energy said it agreed to buy the smart home platform company for $12 per share in cash. NRG Energy fell 8.5% in premarket trading.

- Xponential Fitness (XPOF) was initiated with a buy rating and $29 price target on Tuesday at Citigroup, which said the firm is well positioned to grow within the boutique fitness space. Shares gain 8.5%.

- Silvergate Capital shares slump as much as 14% in premarket trading Tuesday after NBC News reported that Senators including Elizabeth Warren, John Kennedy and Roger Marshall sent a request for information to CEO Alan Lane about the crypto bank’s dealings with Sam Bankman-Fried’s FTX exchange

On Monday, growth at US service providers unexpectedly accelerated in November (well it didn’t really because the Service PMI continued to sink) as a measure of business activity jumped by the most since March 2021, suggesting the largest part of the economy remains resilient.

“Good news is bad news,” Goldman strategist Cecilia Mariotti wrote in a note, pointing to stronger-than-expected US economic data. “Our economists expect Fed Funds rates to peak at around 5-5.25%; a stronger US economy might translate into further pressure on risky assets near-term due to upward pressure on rates.”

As noted yesterday, despite Monday’s rout, the S&P 500 remains on course for its biggest fourth-quarter gain since 1999, but gains have been receding in December after a stellar rally. The benchmark index has now traded lower for three consecutive days, with losses amounting to about 2% so far this month.

“We do not think the economic conditions for a sustained upturn are yet in place,” said Mark Haefele, chief investment officer at UBS Global Wealth Management, noting that growth is slowing and central banks are still raising rates. “We think the inflection point will be reached when a trough in economic activity is in sight and investors can confidently expect rate cuts, rather than a slower pace of hikes.”

The resilient US economy and sticky inflation are countering optimism about a reopening in China, with money market futures and economists suggesting the Fed will need to push rates to a higher peak than previously expected. Swaps showed an increase in expectations for where the Fed terminal rate will be, with the market indicating a peak above 5% in the middle of 2023. The current benchmark sits in a range between 3.75% and 4%.

“Central banks will likely continue to have an outsize impact on stocks in December,” said Kristina Hooper, chief global market strategist at Invesco. “In addition, lowered earnings revisions could exert downward pressure on stocks. Therefore, I expect significant volatility for the month, although the bias is likely upward given historical trends.”

European shares slipped and oil extended declines as traders digested strong US ISM Services PMIs out yesterday. Euro Stoxx 50 falls 0.4%. Energy, financial services and retailers are the worst performing sectors. Here are some of the biggest European movers today:

- Ashtead Technology rises 10% to a record high after the company announced the £20m acquisition of Hiretech, which it expects to result in double-digit earnings accretion in FY23 and generate returns “significantly in excess” of cost of capital in the first full year of ownership.

- SSP shares rise as much as 7.5%, the most since May 25, after the UK catering and concession- services company reported FY results that Morgan Stanley said were “a tad ahead” of the pre-announced expectations.

- Marston’s shares climb as much as 4.4% after the UK pub operator reported FY results, with revenue from continuing operations beating analyst expectations.

- UCB rises as much as 3.1% after getting clarity on the launch of its bimekizumab drug in the US in 2023 should be a catalyst for the stock to re-rate, Barclays writes in a note upgrading the Belgian biopharma to overweight and hiking its PT.

- Aéroports de Paris drops as much as 15% after an offering of 3.87m shares by Royal Schiphol Group priced at €133 apiece, a ~9.9% discount to the last close.

- Scatec falls as much as 5% after Kepler Cheuvreux cut its recommendation for the Norwegian renewable energy firm to hold from buy, citing a lack of short-term triggers for the company’s shares.

- Netcompany shares decline as much as 4.1%, the most since Oct. 19, as Handelsbanken cuts its short-term rating on the IT firm to sell from hold on doubts about its current strategy.

- Telecom Plus declines as much as 2.1% after an offering of 3.5m shares by Chairman Charles Wigoder and others priced at £24 apiece, a discount of 1.4% to the last close.

Earlier in the session, Asian stocks declined as a rebound in Chinese shares lost momentum after unexpectedly strong US economic data renewed concerns that the Federal Reserve will need to push rates to a higher peak than previously expected. The MSCI Asia Pacific Index dropped as much as 1.2%, with Chinese internet firms and Asian chipmakers contributing the most to the benchmark’s drop. Shares in Hong Kong dropped as investors monitored China’s move toward exiting its Covid Zero policy. Gauges in Taiwan, South Korea and Singapore fell while Vietnam’s equity benchmark sank about 4% amid profit taking. Asia’s drop was limited relative to losses in the US, where about 95% of the S&P 500’s companies were in the red. Stocks in Japan edged up as investors weighed dovish remarks from Bank of Japan Governor Haruhiko Kuroda. Still, Asian equities are caught in a tug-of-war between a slowing global growth outlook and optimism around China’s reopening, with expectations of regional earnings estimates taking a further hit. “Near-term earnings downgrades are likely to persist amid weak macro and industrial data across the region and sectors,” Goldman Sachs strategists including Timothy Moe wrote in a note. Asian stocks were headed toward a technical bull market up until Monday, mainly driven by optimism over China’s easing restrictions. Beijing announced it will scrap Covid testing requirements for most public venues.

Japanese stocks traded in a narrow band amid lingering concerns over the outlook for US monetary policy and the impact of the stronger dollar and weaker yen. The Topix Index rose 0.1% to 1,950.22 as of market close Tokyo time, while the Nikkei advanced 0.2% to 27,885.87. Mitsui & Co. contributed the most to the Topix Index gain, increasing 2%. Out of 2,164 stocks in the index, 801 rose and 1,264 fell, while 99 were unchanged. “While the yen has been strengthening since November, the recent slight halt to the appreciation of the yen is a positive factor for corporate earnings performance,” said Ayako Sera, a market strategist at Sumitomo Mitsui Trust Bank Ltd.

Australian stocks also declined, with the S&P/ASX 200 index falling 0.5% to close at 7,291.30, weighed by banks and mining shares, after Australia’s central bank raised its key interest rate for an eighth consecutive month and said it expects to tighten policy further as it seeks to cool the hottest inflation in three decades. In New Zealand, the S&P/NZX 50 index fell 0.4% to 11,631.60.

In FX, the Bloomberg Dollar Spot Index was largely unchanged on the day as investors weighed the possibility that the Fed will need to keep raising rates faster than other central banks, after a jump in ISM services data on Monday and last week’s strong jobs reading suggested that ongoing inflation risks will require more hikes (this of course will change when first PPI then CPI both miss over the next two weeks).

- The yen recovers from a fall to the day’s low of 136.29 yen, after Governor Haruhiko Kuroda said the Bank of Japan will continue its monetary easing even if wages rise 3%, while the Australian dollar gained after the RBA raised its key interest rate to a 10-year high and said it expects to tighten policy further. Easing of Covid testing requirements in Beijing also boosted risk assets

- The euro inches up above 1.05, holding close to a five-month high of 1.0595 touched on Monday. EUR/USD one- week implied volatility rises to 12.97%, its highest since Nov. 16, as investors prepare for the potential of big currency moves after next week’s FOMC meeting

- The yuan halted five straight days of gains as the dollar strengthened after upbeat US data bolstered the case for more Federal Reserve rate hikes to counter inflation. China’s government bond yields rose tracking a selloff in the credit market. USD/CNH rose 0.2% at 6.9893; USD/CNY gains 0.5% to 6.9917. The offshore yuan had risen as much as 0.4% earlier in the session after Beijing said that negative Covid tests would no longer be needed to enter a range of public venues

In rates, Treasuries slightly richer across the curve, with gains led by front-end and belly following a wider bull-steepening rally in gilts. The 10-year Treasury yield slipped to 3.56%, still holding near the 3.61% hit after Monday’s ISM reading added fuel to traders’ bets on how high Fed interest rates might ultimately go. The two-year Treasury yield falls 2.5 basis points to 4.36%. The 2s10s spread slightly steeper on the day, rebounding from new cycle lows reached Monday. Treasury yields richer by as much as 2.5bp across front-end of the curve, steepening 2s10s by 1.5bp on the day after the spread dropped below -82bp Monday; 10-year yields around 3.56% with bunds outperforming by 2bp in the sector. The Gilt curve is little changed with 2s10s widening 4.1bps. Treasury curve bear steepens.

In commodities, WTI and Brent futures were consolidating after yesterday’s ISM-induced declines which saw the most liquid contract settle lower by almost USD 3/bbl a piece; however, pressure has resumed as the morning progresses as WTI drifts 1.2% lower to trade near $76.01. Spot gold is flat under USD 1,775/oz with some overnight resistance seen near that level, while the 200 DMA resides at 1,794/oz and the 21 DMA at 1,757.90/oz. Base metals are mixed, in-fitting with the cautious risk tone and swings in the Dollar, with 3M LME still under the USD 8,500/t mark but within a contained range.

Looking to the day ahead now, and data releases include German factory orders for October, the November construction PMIs from Germany and the UK, and the US trade balance for October. Otherwise, the US Senate run-off election in Georgia will be taking place.

Market Snapshot

- S&P 500 futures up 0.1% to 4,008.75

- STOXX Europe 600 down 0.2% to 440.64

- MXAP down 0.9% to 157.60

- MXAPJ down 1.3% to 513.83

- Nikkei up 0.2% to 27,885.87

- Topix up 0.1% to 1,950.22

- Hang Seng Index down 0.4% to 19,441.18

- Shanghai Composite little changed at 3,212.53

- Sensex down 0.3% to 62,645.63

- Australia S&P/ASX 200 down 0.5% to 7,291.27

- Kospi down 1.1% to 2,393.16

- German 10Y yield down 1.1% to 1.86%

- Euro little changed at $1.0487

- Brent Futures up 0.2% to $82.82/bbl

- Gold spot up 0.2% to $1,771.99

- U.S. Dollar Index little changed at 105.33

Top Overnight News from Bloomberg

- The year-end holidays are failing to lift the glum outlook for trade as conditions continue to deteriorate across the world’s factories and ports. At the start of December, all four Bloomberg Trade Tracker sentiment gauges were below average, with two even lower in below-normal territory

- European Central Bank Chief Economist Philip Lane said consumer-price growth is probably near its zenith, while acknowledging that borrowing costs will be raised again

- German factory orders rose in October, a sign of hope for manufacturers in Europe’s largest economy as they struggle with inflation and elevated energy costs due to Russia’s war in Ukraine

- China is reporting fewer Covid-19 cases as a wave that started to accelerate last month appears to be tailing off amid a pullback in the sweeping testing regime that saw a negative result needed to even enter a public park

- China has taken several significant steps recently to reverse the country’s worst property slump in modern history, leaving economists searching for signs of turnaround clues. Home sales, land purchases, new housing starts and developer financing will all be key to showing how well the sector is able to recover in the coming year, economists told Bloomberg

A more detailed look at global markets courtesy of Newsquawk

Asia-Pacific stocks were somewhat mixed with early headwinds from Wall St where risk assets were pressured as yields and the dollar gained following strong ISM Services PMI data which stoked concerns for a more aggressive Fed. However, some of the initial losses in the regional bourses were reversed owing to further China reopening efforts. ASX 200 was subdued amid mixed data releases and after the RBA rate decision where the central bank delivered an 8th consecutive rate increase, as well as signalled further hikes ahead. Nikkei 225 was kept afloat after BoJ Governor Kuroda reaffirmed sticking with current monetary policy but with gains capped by mixed Household Spending data and the largest decline in real cash earnings in 7 years. Hang Seng and Shanghai Comp were choppy with initial pressure amid the uninspired mood across the region although the losses were briefly pared owing to further reopening efforts in which Shanghai and Beijing scrapped COVID test requirements for more public venues, while reports also noted that China could announce 10 supplementary COVID measures as soon as Wednesday and could downgrade COVID to a category B management as early as January.

Top Asian News

- Beijing city government said it no longer requires negative PCR test results for people entering supermarkets and commercial buildings, while it still requires a negative test result to enter internet cafes, bars, KTV lounges, gyms and elderly care institutions. It was also later reported that the Beijing capital airport no longer requires negative COVID test results from people entering the airport, according to Reuters.

- PBoC’s recent RRR cut could push the 5-year LPR lower this month, according to Shanghai Securities News.

- BoJ Governor Kuroda said it is premature to debate specifics on the BoJ’s monetary policy framework, when asked about board member Tamura’s comments calling for a review of the current framework, while Kuroda added that when the achievement of the inflation target comes into sight, the BoJ will likely debate a path toward an exit from easy policy. Kuroda also said the benefits of the current monetary policy currently outweigh the costs and that the BoJ will continue QQE to ensure companies can smoothly raise wages.

- RBA hiked rates by 25bps to 3.10%, as expected, while it repeated that the board expects to increase interest rates further over the period ahead but is not on a pre-set course and that inflation in Australia is too high. RBA said the board remains resolute in its determination to return inflation to target and will do what is necessary to achieve that, while its priority is to re-establish low inflation and return inflation to the 2%–3% target over time.

In Europe it has been a choppy session thus far across equities as the region looks for direction following the mixed APAC handover and after the post-ISM losses. Currently, European bourses are lower by circa. 0.5% having dipped a touch heading into US trade with fundamental drivers limited. Sectors in Europe are predominantly in the red with a slight defensive tilt, with Utilities, Media, Telecoms, Food & Beverages and Optimised Goods in the green, whilst Energy, Autos, Retail and Financial services reside at the foot of the bunch. US equity futures move between mild losses and gains in search of the next catalyst, with a relatively broad-based action seen across the ES, NQ, YM, and RTY. TSMC (TSM) is to more than triple its investment in Arizona, US to USD 40bln, via FT; will, on Tuesday, announce plans for a second fab to manufacture 3NM/N3 chips from 2026, according to FT sources.

Top European News

- ECB’s Lane said he is confident that the EZ is near the peak of inflation but more hikes are needed, and added that inflation peak may have been reached or will come in early 2023 and the bulk of the work has been done. Re. rates: “… when we take future interest rate decisions, including in December, we should take into account the scale of what we have already done. So the basis for the decision will be different.”

- ECB’s Herodotou said does not see a “hard-landing” in the Eurozone economy; no material de-anchoring of inflation expectations. There will be another hike but we are very close to the neutral rate, via Reuters.

- Barclaycard UK November consumer spending rose 3.9% Y/Y vs prev. 3.5% increase in October.

FX

- DXY briefly eclipsed Monday’s best to a 105.50 peak before fading in limited newsflow and as UST yields ease.

- Action which comes to the modest benefit of peers, ex-CAD given softer benchmark crude prices and pre-BoC; USD/CAD 1.3600.

- Aussie is the modest outperformer following a 25bp RBA hike and guidance for further inflation-justified tightening, AUD/USD 0.673+ at best.

- JPY has derived some modest benefit from the USD pullback, though USD/JPY remains near Monday’s peak.

- GBP and EUR were unfased by the morning’s data points, while remarks from ECB’s Lane are notable but haven’t altered December’s pricing much.

- PBoC set USD/CNY mid-point at 6.9746 vs exp. 6.9773 (prev. 7.0384)

- Norges Bank Regional Network (Q4): output index 6-months ahead -0.57 (Prev. -0.16).

FX

- Core benchmarks are little changed overall, with USTs and Bunds marginally outpacing their UK peer at present.

- However, this relative outperformance is limited in nature and has eased from best levels, while EGBs/Gilts have absorbed the morning’s supply well thus far.

Commodities

- WTI and Brent futures were consolidating after yesterday’s ISM-induced declines which saw the most liquid contract settle lower by almost USD 3/bbl a piece; however, pressure has resumed as the morning progresses, benchmarks lower by circa. USD 1/bbl.

- Spot gold is flat under USD 1,775/oz with some overnight resistance seen near that level, whilst the 200 DMA resides at 1,794/oz and the 21 DMA at 1,757.90/oz.

- Base metals are mixed, in-fitting with the cautious risk tone and swings in the Dollar, with 3M LME still under the USD 8,500/t mark but within a contained range.

- Russian Deputy PM Novak says they may reduce oil production, but not by much, via Tass. Domestic oil production in December will remain at November’s level.

Geopolitics

- Kyiv reportedly used unmanned drones to strike two bases in the heart of Russia, while the drones were launched from Ukrainian territory and two planes were destroyed at one of the Russian bases with several more damaged, according to NYT citing a Ukrainian official.

- North Korea ordered its military to fire artillery into the sea in response to South Korean drills, according to KCNA.

- North Korea fires 10 additional artillery shots in the maritime buffer zone… A total of 100 rounds, according to Yonhap.

- China’s Defence Ministry dismissed a Pentagon report from last month which stated that China would likely have a stockpile of 1,500 nuclear warheads by 2035 if it continues at the current pace of its nuclear build-up, while China dismissed the report as unfair “gesticulation” and speculation, according to Reuters.

US Event Calendar

- 08:30: Oct. Trade Balance, est. -$80b, prior -$73.3b

DB’s Jim Reid concludes the overnight wrap

I’ve always thought that my career would be protected from the invasion of tech, robots and AI, by the fact that no one would ever want to read the “Early Morning Robot”. However I was shocked to read yesterday that the OpenAI foundation have created a bot that would have scored top marks in an academic written assessment. It was even able to write limericks. No doubt it has decent knees and a strong back too. So this morning I’m wondering what purpose I actually serve in life. I’m sure a robot would bring up my kids better too.

It doesn’t need a robot to tell you that markets got the week off to a rocky start yesterday, with solid US data releases knocking back investors’ hopes that the Fed might become more dovish in the days, weeks and months ahead. In particular, the ISM services index painted a very different picture to the manufacturing contraction last week, with the 56.5 reading surpassing the estimates of all 60 economists on Bloomberg. That built on the more positive economic signals from last Friday’s jobs report. The S&P 500 (-1.79%) lost further ground as markets grew sceptical that the Fed would be easing off any time soon with numbers like these.

One of our big calls for next year is that something normally breaks when the Fed has a hiking cycle. That’s certainly been the case over the last 50 years and we’re not sure why this time should be different given the illiquidity and leverage in the system. One of our areas of concern has been the shadow banking system and more specifically private markets. It was interesting that news last week that Blackstone has limited redemptions from one of its private real estate funds caused some nerves in private markets. That follows several warnings by high-profile private capital managers and investors of portfolio write-downs at year end. To further discuss the general topic, Luke Templeman on my team will host a webinar this Thursday at 2pm UK time. He will discuss the risks in the private capital market and how they may spread in 2023 and beyond. You can register here and see the original report on risks in private markets here.

Back to markets and in terms of the specifics of the ISM release, the 56.5 print in November was a big contrast with consensus expectations, which had been for a 53.5 reading that would’ve been the lowest since May 2020. Furthermore, the employment component moved out of contractionary territory with a 51.5 reading, which echoed the better-than-expected numbers in the jobs report, while the prices paid component remains still elevated at 70, lest we forget the still inflationary backdrop. In addition just as the ISM services surprised on the upside, October’s factory orders similarly surprised in a positive direction at +1.0% (vs. +0.7% expected), whilst the final composite PMI was also revised up a tenth from the flash reading to 46.4.

In light of the various releases, expectations of the Fed terminal rate priced for May 2023 moved up by +9.5bps on the day to 5.01%, crossing the 5% threshold again. That’s a noticeable shift from where it was just before Friday’s jobs report, when it hit a low of 4.83%, and means that most of the moves lower after Chair Powell’s Wednesday speech have now reversed. Meanwhile, pricing for end-2023 rose by an even larger +16.8bps to 4.60%, as markets priced in that policy will be restrictive for longer with data like this. In turn, this all prompted a big shift higher in Treasury yields as well, with the 10yr yield up +8.7bps on the day to 3.57%, and real yields up by +12.0bps to 1.17%. In the meantime, the various releases saw the dollar index strengthen in the aftermath, moving up from its weakest intraday level since June to gain +0.74% on the day. This morning in Asia, yields on 10yr USTs are fairly stable, trading at 3.58%.

The positive data meant equities lost decent ground yesterday thanks to the concern about further rate hikes. To be fair, the S&P 500 had already opened lower, but the ISM services reading saw it take another leg down to close the day with a -1.79% loss. The declines were broad-based across various sectors, but the cyclical industries performed worst of all, with consumer discretionary (-2.95%) and energy (-2.94%) the biggest laggards. The picture was also subdued in Europe, where the STOXX 600 fell -0.33%.

Overnight, we’ve had some further central bank news after the Reserve Bank of Australia (RBA) delivered a third consecutive interest rate hike of 25bps, taking the official rate to 3.1% – the highest level since 2012 after the fastest tightening cycle in a generation. Following the announcement, RBA Governor Lowe said the board “expects to increase interest rates further over the period ahead”. The comments supported the Australian dollar (+0.49%), pushing the currency to $0.673, while 2yr bond yields jumped 9bps to 3.07%.

Elsewhere in Asia stock markets are mixed this morning after Wall Street sold off overnight. As I type, the Hang Seng (-0.93%) and the Hang Seng Tech index (-1.92%) are both trading in negative territory despite Beijing easing some Covid test requirements for the city. Meanwhile, the KOSPI (-0.71%) is weak while the Nikkei (+0.37%) and the CSI (+0.55%) are higher in early trading with the Shanghai Composite (-0.08%) struggling to gain traction. In overnight trading, US stock futures are indicating a mixed start with contracts on the S&P 500 (+0.06%) just above flat while those on the NASDAQ 100 (-0.04%) are oscillating between gains and losses.

Early morning data showed that household spending in Japan (+1.2% y/y) advanced for a 5th consecutive month in October and slightly better than the market estimate of 0.9% as Covid cases continued to decline. At the same time, elevated inflation saw Japan’s real wages (-2.6% y/y) post their biggest fall in more than seven years (v/s -2.2% expected). That compares with a downward revised fall of -1.2% in the preceding month.

Back in Europe, there wasn’t a great deal of newsflow yesterday, with the final composite PMIs painting a very similar picture to the flash prints. Indeed, the Euro Area composite PMI was completely unchanged from the flash reading at 47.8. We didn’t get much in the way of ECB headlines either, although Ireland’s central bank Governor Makhlouf said that a 50bp hike “is about where we’ll end up”. That’s in line with market expectations for next week’s meeting, which have continued to drift closer to the 50bps point over the last month, with 53.9bps currently priced in.

Sovereign bonds had a divergent performance against this backdrop, with yields on 10yr bunds up +2.6bps on the day, yields on 10yr OATs up +0.9bps, but yields on 10yr BTPs down -1.2bps. Gilts were an outperformer however, which followed weekend comments from the MPC’s Dhingra suggesting that the BoE should not raise rates as far as the 4.5% markets are pricing. 10yr yields fell -4.8bps.

Looking ahead, today is an important one in US politics as the Georgia Senate run-off election takes place. This doesn’t have quite the significance it did two years ago, since the Democrats already have 50 seats and will control the Senate regardless of the result thanks to Vice President Harris’ casting vote. But it will still have important implications, since a 51-49 margin means the Democrats could still win a Senate vote even if they lost one of their number like Senator Joe Manchin. Furthermore, since Senate seats only come up every 6 years with just a third of the chamber elected each time, a victory for either side would make it easier for them to gain control in the 2024 and 2026 elections as well, since that Georgia seat wouldn’t be up for election again until 2028.

To the day ahead now, and data releases include German factory orders for October, the November construction PMIs from Germany and the UK, and the US trade balance for October. Otherwise, the US Senate run-off election in Georgia will be taking place.10,10219