BY TYLER DURDEN …

MONDAY, MAY 15, 2023 – 07:15 AM …

After several busy weeks, and with some 90% of S&P companies having already reported Q1 earnings, newsflow slows down and there are no blockbuster US data releases, but US retail sales (tomorrow) and a selection of US housing data will be the highlights. Across the globe, we will also see the monthly China economic activity data dump (tomorrow), GDP and CPI reports from Japan (Wednesday and Friday), along with labor market reports in the UK (tomorrow). In addition, there are a lot of central bank speakers, especially from the Fed. Fed Chair Powell and ECB President Lagarde both speak on Friday with the latter also up tomorrow.

Elsewhere the latest G7 summit starts on Friday in Hiroshima and earnings season still lingers with notable companies reporting being US retailers Walmart and Home Depot, along with China’s tech giants Alibaba and Tencent.

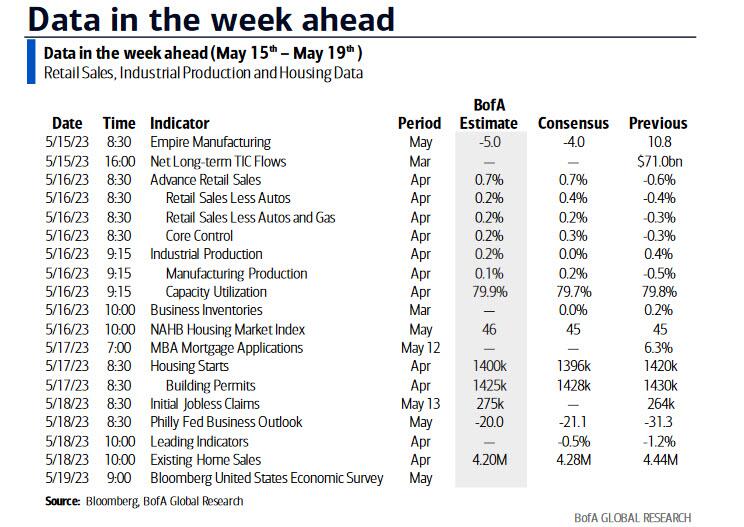

Taking a more detailed look at the data, DB’s Jim Reid starts with his preview of US retail sales tomorrow, where DB economists expect the headline to print at +0.7% in April, up from -0.6% previously, or +0.5% vs -0.4% ex autos (we will have a detailed retail sales preview later in the day). Headline will likely be boosted by strong auto sales in the month. The gain in ex-autos sales is likely to be gas price related while economists expect a flat reading on retail control (unch. vs. -0.3%), which is the direct input into GDP for goods spending. So consumption is grinding lower after a strong start to the year, something we detailed over the weekend in “There Goes The US Consumer: Card Data Reveal First Drop In Household Spending In Two Years As Upper-Income Wages Tumble, Unemployment Benefits Soar.” Investors will also get a read on the US consumer from US retailers which report earnings, including Walmart (Thursday), Target (Wednesday) and Home Depot (tomorrow).

Tomorrow’s NAHB housing market index (DB at 44 vs. 46) starts the week for US housing data and will be followed by Wednesday’s housing starts and permits and then Thursday’s existing home sales.

Thursday’s jobless claims will be more important than usual for a couple of reasons. Firstly it is the survey week for the next payrolls release and secondly we saw it confirmed on Friday that a decent slug of the recent rise in claims were likely due to fraudulent filings in Massachusetts. This state seems to have accounted for around half the +23% rise in the 4-week moving average claims number from the late January lows. The 4-week moving average for continuing claims is up around 10% this year so the labor market is easing but not quite as much as the raw claims numbers had suggested.

{kind=link}

In Europe, the UK labor market data tomorrow will be interesting following last week’s twelfth consecutive BoE meeting hike. Whether the data shows persistent wage pressures, following the last hot print, will likely contribute to whether a pause is feasible at the next meeting on June 22, although another round of wages and inflation data will be due by then as well. The house view is that they will hike another 25bps in June which will be the last for the cycle but with the risks that there’ll be more. Elsewhere in Europe, key indicators include the ZEW survey (tomorrow) and the PPI report (Friday) for Germany and Q1 GDP, trade balance for March (tomorrow) and industrial production (today) for the Eurozone.

This week will also be a busy one for the major Asian economies. Starting with Japan, Q1 GDP will be released on Wednesday, trade balance data on Thursday, and the CPI report on Friday.

In China, investors will be focused on the latest economic activity signals tomorrow, with the release of retail sales, industrial production and property investment data. Amid base effects, our economists expect +11% and +21% YoY growth in industrial production and retail sales, respectively (vs 3.9% and 10.6% in March). The industrial production print and its contrast with retail sales will be especially in focus given flailing momentum in the former. New home prices data are due on Wednesday.

China will also be in the spotlight for corporate earnings this week. Its tech giants, including Alibaba (Thursday), Tencent (Wednesday) and Baidu (Tuesday) will be among the most anticipated reports. The full day-by-day week ahead in at the end as usual.

Q1 earnings season is in its final stages, with 80-90% of companies having reported in the US and in Europe. Earnings growth came in better than consensus expected, at -3% y/y in the US, and +3% y/y in Europe, which is a positive surprise factor of 7% and 10% vs IBES estimates, respectively. The low hurdle rate entering the reporting season, combined with the improving fundamentals during the quarter, has likely helped S&P500 blended EPS inflect higher. The last week of earnings as usual focuses on retailers, and we will hear from Walmart (Thursday), Target (Wednesday) and Home Depot (tomorrow).

Below is a day-by-day calendar of events courtesy of DB:

Monday May 15

- Data: US May Empire manufacturing index, Japan April PPI, machine tool orders, Italy March general government debt, Eurozone March industrial production, Canada March wholesale trade sales, April housing starts, existing home sales

- Central banks: Fed’s Bostic, Kashkari and Cook speak, ECB’s Nagel speaks, BoE’s Pill speaks

- Earnings: Siemens Energy, Mitsubishi UFJ Financial, Sumitomo Mitsui, Mizuho, Catalent

Tuesday May 16

- Data: US May New York Fed services business activity, NAHB housing market index, April retail sales, industrial production, capacity utilization, March business inventories, China April retail sales, industrial production, property investment, UK Q1 output per hour, March average weekly earnings, employment change, April payrolled employees monthly change, Germany and Eurozone May ZEW survey, Eurozone Q1 GDP, employment, March trade balance, Canada April CPI, March manufacturing sales

- Central banks: Fed’s Mester, Logan and Williams speak, Fed’s Barr testifies before House Financial Services Committee, ECB’s Lagarde and Makhlouf speak

- Earnings: Home Depot, Baidu, Vodafone

- Others: Joe Biden meets with Congressional Republicans to try to hammer out a deal on the debt ceiling. As covered above, this will be the key theme for the week. We will also see industrial production and retail sales numbers out of China (will that consumer-led revival materialize?) UK employment data, the German ZEW survey, US retail sales and Canadian CPI. ECB Chief Christine Lagarde will be providing comment, as will the ECB’s Makhlouf and a slew of Fed speakers that includes Mester, Barr, Williams, Goolsbee and Bostic.

Wednesday May 17

- Data: US April housing starts, building permits, China April new home prices, Japan Q1 GDP, Japan March capacity utilization, Italy March trade balance, France Q1 ilo unemployment rate, EU27 April new car registrations

- Central banks: Fed’s Bostic and Goolsbee speak, ECB’s Guindos speaks

- Earnings: Target, TJX, Cisco, Take-Two, Tencent, Siemens

- Other: Wednesday: Preliminary 1st quarter GDP data for Japan will kick off a relatively quiet day. The market is looking for a read of 0.2% q-o-q for GDP and 2.1% y-o-y for the price deflator. We will get US housing numbers for April later in the day where starts are seen falling slightly to 1400 for the month. De Cos, Elderson Centeno, Rehn and Guindos will all be in action for the ECB.

Thursday May 18

- Data: US May Philadelphia Fed business outlook, April leading index, existing home sales, initial jobless claims, Japan April trade balance

- Central banks: Fed’s Jefferson and Logan speak, Fed’s Barr testifies before Senate Banking Committee, BoE’s Pill speaks, BoC’s Financial System Review

- Earnings: Alibaba, Walmart, Applied Materials, SQM, BT, easyJet

- Other: Thursday is Aussie jobs Day. The expectation is for 25,000 new positions added in April with the unemployment rate to remain steady at 3.5% and participation also steady at 66.7%. US initial jobless claims will be released later in the day. Expectation there is for a figure of 252,000, well down on the prior read of 264,000. We will also get the Philadelphia Fed’s business outlook for May and the Bank of Canada’s Financial System Review. In terms of central bank speakers, human headline Huw Pill will be in action, as will BOE Governor Andrew Bailey, De Guindos from the ECB and the Fed’s Jefferson, Barr and Logan will also be speaking.

Friday May 19

- Data: UK May GfK consumer confidence, Japan April CPI, March tertiary industry index, Germany April PPI, Canada March retail sales

- Central banks: Fed’s Powell, Williams and Bowman speak, ECB’s Lagarde, De Cos and Schnabel speak, BoE’s Haskel speaks

- Earnings: Deere

- Other: Kiwi trade balance numbers start us off on Friday. Bloomberg provides no estimates for this, but another atrocious number seems a safe bet given recent form. Japanese CPI figures will be out next with the market expecting prices to have risen 3.5% y-o-y in April (up three ticks from the previous month). Out of the UK we will get consumer confidence figures (likely diabolical) and the results of the Bloomberg economic survey, while in Germany we will see April PPI figures and over in the US we will also get results for the Bloomberg economic survey. The Bank of England’s Haskell will be speaking, as will the Fed’s Williams and Bowman. Later on Jerome Powell will be speaking on a panel with Ben Bernanke, while from the ECB we will hear from Lagarde, Schnabel and de Cos.

* * *

Finally, focusing on just the US, Goldman writes that the key economic data releases this week are retail sales on Tuesday and the Philly Fed manufacturing index on Thursday. There are many speaking engagements from Fed officials this week, including Chair Powell; Vice Chair Nominee Jefferson; governors Cook, Barr, and Bowman; and presidents Bostic, Goolsbee, Kashkari, Mester, Williams, and Logan.

Monday, May 15

- 07:30 AM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will participate in an interview with CNBC. On April 20, Bostic said, “Our policy works with the lag. We’ll have moved firmly into restrictive space. And then I think it’s time for us to let the restrictive action work its way through. And that will take some time.”

- 08:30 AM Chicago Fed President Goolsbee (FOMC voter) speaks: Chicago Fed President Austan Goolsbee will participate in an interview with CNBC. On May 10, Goolsbee said, “You don’t want to land the plane nose down. So we’re trying to balance off — can we slow the inflation without sending it into a recession…We’ve had some promising indicators on that front, but it’s always a possibility.” On May 8, he said, “I am certainly getting vibes…in the market and in the business context that a credit crunch or, at least, a credit squeeze, is beginning.”

- 08:30 AM Empire State manufacturing survey, May (consensus -4.0, last +10.8)

- 08:45 AM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will deliver welcoming remarks at the Atlanta Fed’s annual financial markets conference.

- 09:15 AM Minneapolis Fed President Kashkari (FOMC voter) speaks: Minneapolis Fed President Neel Kashkari will participate in a moderated discussion at the ACEC’s Minnesota Transportation Conference & Expo. Q&A with audience is expected. On May 11, Kashkari said, “Inflation has come down but it’s still well above our 2% target. We have seen some softening in wage growth nationally, but it’s very mixed…We’ve been surprised at how high it got, we’ve been surprised at how persistent it’s been. And it’s coming down – there is some evidence that it’s coming down. But so far it’s been pretty darn persistent. That means we’re going to keep at it for an extended period of time.”

- 02:00 PM Atlanta Fed President Bostic (FOMC non-voter) speaks: Atlanta Fed President Raphael Bostic will participate in an interview with Bloomberg TV at 2:00 PM and hold a media Q&A at the Atlanta Fed’s financial markets conference at 3:00 PM.

- 05:00 PM Fed Governor Cook speaks: Fed Governor Lisa Cook will deliver a commencement address at the U.C. Berkeley Spring 2023 Economics Commencement. Speech text is expected. On April 21, Cook said, “Currently, with the federal funds rate target near 5%, I am looking at what rate will be sufficiently restrictive to bring inflation down to 2%, over time…If tighter financing conditions are a significant headwind on the economy, the appropriate path of the federal funds rate may be lower than it would be in their absence. But if data show continued strength in the economy and slower disinflation, we may have more work to do.”

Tuesday, May 16

- 08:15 AM Cleveland Fed President Mester (FOMC non-voter) speaks: Cleveland Fed President Loretta Mester will discuss the economic and policy outlook at a Global Interdependence Center event hosted by the Central Bank of Ireland. Speech text and a Q&A with the audience are expected. On April 20, Mester said, “I anticipate that monetary policy will need to move somewhat further into restrictive territory this year, with the fed funds rate moving above 5% and the real fed funds rate staying in positive territory for some time. Precisely how much higher the federal funds rate will need to go from here and for how long policy will need to remain restrictive will depend on economic and financial developments.”

- 08:30 AM Retail sales, April (GS +1.3%, consensus +0.8%, last -0.6%); Retail sales ex-auto, April (GS +0.8%, consensus +0.4%, last -0.4%) ;Retail sales ex-auto & gas, April (GS +0.4%, consensus +0.2%, last -0.3%); Core retail sales, April (GS +0.5%, consensus +0.3%, last -0.3%): We estimate core retail sales rebounded by 0.5% in April (ex-autos, gasoline, and building materials; mom sa). Our forecast reflects a rebound in high-frequency consumer spending data, including in mall-based categories such as clothing stores. However, we expect another month of flat-to-down grocery spending due to the expiration of pandemic food stamp benefits. We estimate a 1.3% rise in headline retail sales, reflecting higher auto sales and gasoline prices.

- 09:15 AM Industrial production, April (GS +0.2%, consensus flat, last +0.4%); Manufacturing production, April (GS +0.3%, consensus +0.1%, last -0.5%); Capacity utilization, April (GS 79.8%, consensus 79.7%, last 79.8%): We estimate industrial production increased 0.2% in April, as stronger auto production is partially offset by weaker natural gas utilities. We estimate capacity utilization remained at 79.8%.

- 10:00 AM Business inventories, March (consensus flat, last +0.2%)

- 10:00 AM NAHB housing market index, May (consensus 45, last 45)

- 10:00 AM Fed Governor Barr speaks: Fed Vice Chair for Supervision Michael Barr will testify before the House Financial Services Committee in its Semiannual Hearing on Supervision and Regulation. Speech text will be available.

- 12:15 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will participate in a moderated discussion on the economic outlook and monetary policy at an event hosted by the University of the Virgin Islands. On May 9, Williams said, “We haven’t said we are done raising rates…We’ve made incredible progress” but “if additional policy firming is appropriate, we’ll do that.” He added, “In my forecast I see a need to keep a restrictive stance of policy in place for quite some time to make sure we really bring inflation down from 4% all the way to 2%. I do not see in my baseline forecast any reason to cut interest rates this year.”

- 02:30 PM Chicago Fed President Goolsbee (FOMC voter) speaks: Chicago Fed President Austan Goolsbee will participate in an interview with Bloomberg TV.

- 03:15 PM Dallas Fed President Logan (FOMC voter) speaks: Dallas Fed President Lorie Logan will moderate a panel discussion at the Atlanta Fed’s Financial Markets Conference. Q&A with audience is expected. On April 20, Logan said, “Over the past six weeks, I’ve also been closely watching the effects of stresses in the banking system—both on the macroeconomy and on local communities, especially here in Texas where small and midsize banks are so important. Smaller banks are particularly significant in small business, rural, middle-market, and commercial real estate lending.”

- 07:00 PM Atlanta Fed President Bostic (FOMC non-voter) and Chicago Fed President Goolsbee (FOMC voter) speak: Atlanta Fed President Raphael Bostic and Chicago Fed President Austan Goolsbee will participate in a moderated discussion on the economic outlook during the Atlanta Fed’s annual financial markets conference. On May 10, Goolsbee said, “You don’t want to land the plane nose down. So we’re trying to balance off — can we slow the inflation without sending it into a recession…We’ve had some promising indicators on that on that front, but it’s always a possibility.” On May 8, he said, “I am certainly getting vibes…in the market and in the business context that a credit crunch or, at least, a credit squeeze, is beginning.”

Wednesday, May 17

- 08:30 AM Housing starts, April (GS -1.1%, consensus -1.4%, last -0.8%): Building permits, April (consensus flat, last -7.7%)

Thursday, May 18

- 08:30 AM Initial jobless claims, week ended May 13 (GS 240k, consensus 252k, last 264k); Continuing jobless claims, week ended May 6 (consensus 1,818k, last 1,813k): We estimate that initial jobless claims fell to 240k in the week ended May 13. Last week’s jump in initial claims partly reflected fraudulent filings in Massachusetts. Our forecast assumes that those fraudulent filings—which we estimate could be boosting the level of claims by roughly 20-30k—are curtailed. While the annual seasonal factor revisions that took place last month appear to have resolved most of the seasonal distortions in initial claims, we believe the revisions may have intensified the distortions in continuing claims. Those distortions have likely contributed to the net decline over the last few prints, and we estimate they could exert a cumulative drag on the level of continuing claims of up to 400k between April and September.

- 08:30 AM Philadelphia Fed manufacturing index, May (GS -16.0, consensus -19.8, last -31.3): We estimate that the Philadelphia Fed manufacturing index rebounded 15.3 points to -16 in May, reflecting the gradual rebound in East Asian trade and industrial activity following weakness in the winter.

- 09:05 AM Fed Governor Jefferson speaks: Fed Governor Philip Jefferson will deliver a speech on the economic outlook at the National Association of Insurance Commissioners (NAIC) International Insurance Forum. Speech text is expected. On May 9, Jefferson said, “The economy has started to slow in an orderly fashion…I am of the view that inflation will start to come down and the economy will have the opportunity to continue to expand.” President Biden will nominate Jefferson as Vice Chair of the Federal Reserve.

- 09:30 AM Fed Governor Barr speaks: Fed Vice Chair for Supervision Michael Barr will testify before the Senate Banking Committee in its Semiannual Hearing on Supervision and Regulation. Speech text will be made available. Barr released the review of the Fed’s supervision and regulation of Silicon Valley Bank on April 28.

- 10:00 AM Dallas Fed President Logan (FOMC voter) speaks: Dallas Fed President Lorie Logan will deliver a speech, followed by moderated Q&A with audience, at Texas Bankers Association’s annual convention.

- 10:00 AM Existing home sales, April (GS -5.0%, consensus -3.2%, last -2.4%)

Friday, May 19

- 08:45 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will deliver a keynote address at a monetary policy research conference hosted by the Fed.

- 09:00 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will participate in a discussion at the Texas Bankers Association Annual Convention. Speech text and a moderated Q&A are expected. On May 12, Bowman said, “Should inflation remain high and the labor market remain tight, additional monetary policy tightening will likely be appropriate to attain a sufficiently restrictive stance of monetary policy to lower inflation over time. I also expect that our policy rate will need to remain sufficiently restrictive for some time to bring inflation down and create conditions that will support a sustainably strong labor market.”

- 11:00 AM Fed Chair Powell speaks: Fed Chair Jerome Powell and former chair Ben Bernanke will participate in a panel discussion during a monetary policy research conference hosted by the Fed. At the May FOMC meeting, Powell said that he does not expect a recession, unlike the Fed staff, and he made his clearest statement so far that he thinks a soft landing is possible and finds the labor market rebalancing to date encouraging, views that we share. We see this as dovish too—if Powell thinks that a recession is not necessary to solve the inflation problem, he will be reluctant to deliver future hikes that he thinks would materially raise the risk of pushing the economy into a recession.

Source: DB, Goldman, Rabobank, BofA