MONDAY, APR 15, 2024 – 09:00 AM

While back on Friday the market’s attention was mostly on the start of earnings season, this weekend’s events have quickly shift focus and looking forward, the important question now is how Israel might respond to the (scripted) war between Iran and Israel, and whether it could lead to a further escalation in the conflict (it won’t, but just like Iran, Israel will likely fire off a couple of cruise missiles into the desert so as not to appear toothless and call it a day).

A meeting of Israel’s war cabinet ended on Sunday evening without a decision on how Israel would respond, and according to NBC, the war Cabinet will reconvene today. And Reuters reported that the war cabinet favored retaliation, but was divided over the response according to Israeli officials. That followed comments earlier in the day from Benny Gantz, a minister in the war cabinet, who said that Israel will “exact a price from Iran in a way and time that suits us”. And Itamar Ben-Gvir, the national security minister, called for a “crushing attack”. But in the US, reports have indicated that there is more caution about an escalation, and Axios reported that Biden had told Israeli PM Netanyahu that the US wouldn’t support an Israeli counterattack, according to a senior White House official.

Given all this, developments in the Middle East will be the main focus this week, and we know from recent experience that geopolitical tensions can impact the global economy through several channels. Most directly, the effects of higher oil prices will be felt globally, and this is coming at a time when there’s already concern about sticky inflation in several countries. That’s something that could create a dilemma for central banks, as we also found out after Russia’s invasion of Ukraine in 2022. On the one hand, there is the risk that a geopolitical shock hurts growth, bringing forward the timing of rate cuts. Indeed, markets were clearly pricing that risk on Friday, with the chance of a Fed rate cut by June moving up from 24% to 30%, although that’s since moved back to 24% this morning. But then again, if higher oil prices lead to more inflation and there are second round effects on other prices, then that could mean monetary policy has to stay in restrictive territory for longer. So the potential effects can work both ways.

Turning away from geopolitics, we’ll get the chance to hear from several policymakers this week, as numerous officials are gathering in Washington DC for the IMF-World Bank Spring Meetings. Tomorrow, we’ll get the IMF’s latest World Economic Outlook, including their forecasts for the global economy. And over the week, we’ll hear from Fed Chair Powell, ECB President Lagarde, and Bank of England Governor Bailey, among others. This week is also the last opportunity to hear from Fed speakers ahead of the next meeting, as their blackout period begins on Saturday.

Otherwise this week, earnings season will begin to ramp up before it really gets into full flow over the subsequent week. That includes releases from 41 companies in the S&P 500, along with 21 from the STOXX 600, with results from Morgan Stanley, Goldman Sachs, Bank of America, Netflix and Johnson & Johnson.

{kind=link}

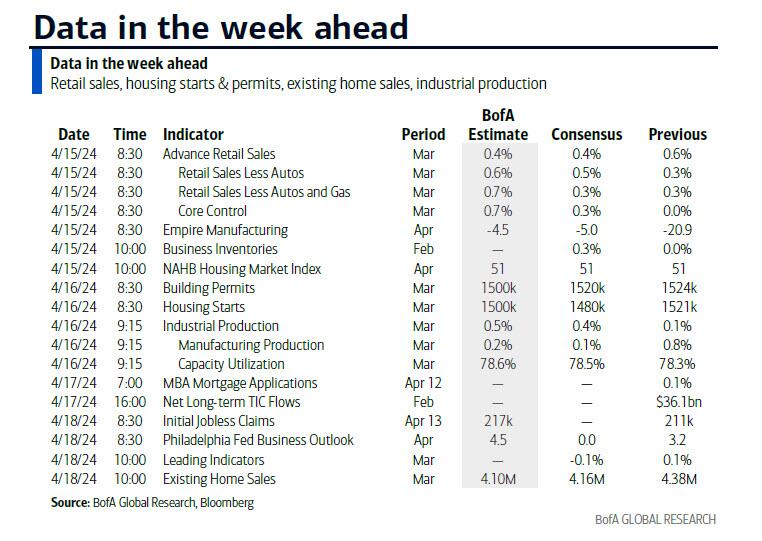

Finally on this week’s data, we’ve got the Q1 GDP release for China out tomorrow, along with their March data for retail sales and industrial production. Meanwhile, there are CPI releases for March in the UK, Japan and Canada, which will also be in focus as markets assess the timing of any monetary policy moves. Then in the US, we’ve also got some more data for March, including retail sales, housing starts, building permits, and industrial production.

{kind=link}

Courtesy of DB, here is a day-by-day calendar of events

Monday April 15

- Data : US March retail sales, February business inventories, April NAHB housing market index, Empire manufacturing index, Japan February core machine orders, Italy February general government debt, Eurozone February industrial production, Canada March housing starts, February manufacturing sales

- Central banks : Fed’s Logan speaks, ECB’s Simkus and Lane speak, BoE’s Breeden speaks, China 1-yr MLF rate

- Earnings : Goldman Sachs

Tuesday April 16

- Data : US March industrial production, capacity utilization, housing starts, building permits, April New York Fed services business activity, UK March jobless claims change, February average weekly earnings, ILO unemployment rate, China Q1 GDP, March home prices, retail sales, industrial production, property investment, Italy February trade balance, Germany and Eurozone April Zew survey, Eurozone February trade balance, Canada March CPI, New Zealand Q1 CPI

- Central banks : Fed Chair Powell, Fed’s Daly and Jefferson speak, ECB’s Rehn, Villeroy and Vujcic speak, BoE’s Bailey and Lombardelli speak

- Earnings : Johnson & Johnson, Bank of America, UnitedHealth, Morgan Stanley, United Airlines

- Other : IMF releases World Economic Outlook

Wednesday April 17

- Data : US February total net TIC flows, UK March CPI, PPI, RPI, February house price index, Japan March trade balance, Canada February international securities transactions

- Central banks : Fed’s Beige Book, Mester and Bowman speak, ECB President Lagarde, ECB’s Cipollone, De Cos and Schnabel speak, BoE’s Bailey, Greene and Haskel speak

- Earnings : ASML, Volvo, Prologis, Abbott Laboratories, Alcoa, Crown Castle

- Auctions : US 20-yr Bond (reopening, $13bn)

Thursday April 18

- Data : US March leading index, existing home sales, April Philadelphia Fed business outlook, initial jobless claims, Japan February Tertiary industry index, Italy February current account balance, EU27 March new car registrations, ECB February current account, Eurozone February construction output

- Central banks : Fed’s Bowman, Williams and Bostic speak, BoJ’s Naguchi speaks , ECB’s Centeno, Simkus and Vujcic speak

- Earnings : TSMC, Netflix, Blackstone

- Auctions : US 5-yr TIPS ($23bn)

Friday April 19

- Data : UK March retail sales, Japan March national CPI, Germany March PPI

- Central banks : Fed’s Goolsbee speaks, ECB’s Nagel speaks, BoE’s Ramsden speaks

- Earnings: Procter & Gamble, American Express, Schlumberger

- Other: India’s general elections begin

* * *

Finally, here is a weekly preview focusing only on the US from Goldman, which notes that the key economic data releases this week are the retail sales report on Monday and the Philly Fed manufacturing index on Thursday. There are several speaking engagements from Fed officials this week, including public appearances by Chair Powell and by Vice Chair Jefferson on Tuesday and by New York Fed President Williams on Monday, Tuesday, and Thursday.

Monday, April 15

- 02:30 AM Dallas Fed President Logan (FOMC non-voter) speaks: Dallas Fed President Lorie Logan will participate in a panel discussion at a conference on gender diversity in the workplace hosted by the IMF and the Bank of Japan in Tokyo. Moderated Q&A is expected. On April 5th, President Logan noted that she believed it was “much too soon to think about cutting interest rates,” and that FOMC participants “should remain prepared to respond appropriately if inflation stops falling.” President Logan emphasized that the FOMC had “time to wait and see the incoming data and see how financial conditions are evolving,” and that “there is no urgency right now” to cut the fed funds rate.

- 08:30 AM Empire State manufacturing survey, April (consensus -5.0, last -20.9); 08:30 AM Retail sales, March (GS +0.5%, consensus +0.4%, last +0.6%); Retail sales ex-auto, March (GS +0.6%, consensus +0.5%, last +0.3%); Retail sales ex-auto & gas, March (GS +0.6%, consensus +0.3%, last +0.3%); Core retail sales, March (GS +0.6%, consensus +0.4%, last flat): We estimate core retail sales rose 0.6% in March (ex-autos, gasoline, and building materials; mom sa). Our forecast reflects a boost from Easter spending but mixed credit card spending data for the month as a whole. We estimate a 0.5% rise in headline retail sales, reflecting lower auto sales and flat-to-down gasoline spending.

- 08:30 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will take part in an interview on Bloomberg Television. On April 11th—after the March CPI report was released—President Williams said that he expected “inflation to continue its gradual return to 2%, although there will likely be bumps along the way, as we’ve seen in some recent inflation readings,” and that he expected “overall PCE inflation to be 2.25% to 2.5% this year, before moving closer to 2% next year.” President Williams also noted that “if the economy proceeds as expected, it will make sense to dial back the policy restraint gradually over time, starting this year.”

- 10:00 AM NAHB housing market index, April (consensus 51, last 51)

- 10:00 AM Business inventories, February (consensus +0.4%, last flat)

- 08:00 PM San Francisco Fed President Daly (FOMC voter) speaks: San Francisco Fed President Mary Daly will participate in a fireside chat at the Stanford Institute for Economic Policy Research. Q&A is expected. On April 12th, President Daly emphasized that “there is … no urgency to adjust the policy rate,” and that she would “need to be fully confident that inflation is on track to come down to 2% … before we would consider a rate cut.” President Daly also noted that there was “a lot of work to do before we can be confident that we have price stability.”

Tuesday, April 16

- 08:30 AM Housing starts, March (GS -1.1%, consensus -2.6%, last +10.7%): Building permits, March (consensus -0.9%, last +2.4%)

- 09:00 AM Fed Vice Chair Jefferson speaks: Fed Vice Chair Philip Jefferson will deliver a keynote address at the International Research Forum on Monetary Policy, hosted by the Fed Board. On February 22nd, Vice Chair Jefferson noted that the FOMC always needed to “keep in mind the danger of easing too much.” At the same time, Vice Chair Jefferson said that “the labor market can change dramatically,” and that the FOMC had to “be careful and we have to try to assess the different shocks that can hit the economy and adjust policy accordingly.”

- 09:15 AM Industrial production, March (GS +0.1%, consensus +0.4%, last +0.1%): Manufacturing production, March (GS +0.3%, consensus +0.2%, last +0.8%)

- Capacity utilization, March (GS 78.3%, consensus 78.5%, last 78.3%): We estimate industrial production rose 0.1%, as weak mining production offsets strong natural gas production and underlying strength in manufacturing activity. We estimate capacity utilization was unchanged at 78.3%.

- 12:30 PM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will moderate a discussion with François Villeroy de Galhau at the Economic Club of New York.

- 01:00 PM Richmond Fed President Barkin (FOMC voter) speaks: Richmond Fed President Thomas Barkin will speak on the economic outlook at the Rotary Club of Winston-Salem. Q&A is expected. On April 11th, President Barkin stressed that “we’re not yet where we want to be” on inflation, but that “the longer arc suggests we are headed in the right direction.” He noted that “we are still in this environment of not high inflation, but higher than target inflation.”

- 01:15 PM Fed Chair Powell speaks: Fed Chair Jerome Powell will participate in a moderated discussion with Tiff Macklem, Governor of the Bank of Canada, at the Washington Forum on the Canadian Economy in Washington, D.C. Q&A is expected. On April 9th, before the March CPI report was released, Chair Powell noted that the recent inflation data did not “materially change” the outlook for monetary policy, and that he expected it would likely be appropriate to start lowering rates “at some point this year.” Still, Chair Powell noted that it was “too soon to say whether the recent [inflation] readings represent more than just a bump.”

Wednesday, April 17

- 02:00 PM Beige Book, April/May FOMC meeting period: The Fed’s Beige Book is a summary of regional economic anecdotes from the 12 Federal Reserve districts. The Beige Book for the March FOMC meeting period noted that activity accelerated somewhat in early 2024 and that firms’ economic outlook for the remainder of the year was generally positive. Businesses reported that consumers had become more sensitive to price increases in early 2024. At the same time, regional labor markets continued to soften and companies were finding it easier to hire and retain workers. In this month’s Beige Book, we look for anecdotes related to possible turning points in regional labor markets and for further commentary on businesses’ inflation expectations over the next few months.

- 05:30 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will take part in a discussion on the Fed and monetary policy in Ohio. Q&A is expected. On April 4th, President Mester said she wanted to “see a couple more months of data” to judge whether inflation had continued to decline toward the Fed’s 2% target. President Mester also noted that if the labor market “were to deteriorate significantly, we have a policy position that we can address that and we can move rates down more swiftly and sooner than in our baseline forecast.”

- 07:15 PM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will participate in a fireside chat at the Institute of International Finance’s Global Outlook Forum dinner in Washington, D.C. Q&A is expected. On April 5th, Governor Bowman noted that “inflation readings over the past two months suggest progress may be uneven or slower going forward,” and that she expected “further progress in bringing inflation down to 2% will be slower this year.” She emphasized that, while not her “baseline outlook,” she continued to “see the risk that at a future meeting we may need to increase the policy rate further should progress on inflation stall or even reverse.”

Thursday, April 18

- 08:30 AM Philadelphia Fed manufacturing index, April (GS 5.2, consensus 2.3, last 3.2): We estimate that the Philadelphia Fed manufacturing index rose 2pt to 5.2 in April, reflecting a boost from the foreign manufacturing rebound and strength in US production and freight activity.

- 08:30 AM Initial jobless claims, week ended April 13 (GS 215k, consensus 215k, last 211k); Continuing jobless claims, week ended April 6 (consensus 1,818k, last 1,817k)

- 09:05 AM Fed Governor Bowman speaks: Fed Governor Michelle Bowman will deliver pre-recorded opening remarks at the 2024 Regional and Community Banking Conference, hosted by the New York Fed. Text is expected.

- 09:15 AM New York Fed President Williams (FOMC voter) speaks: New York Fed President John Williams will take part in a moderated discussion at the Semafor World Economy Summit in Washington, D.C. Q&A is expected.

- 09:15 AM Fed Governor Bowman speaks: Fed Governor Bowman will participate in a fireside chat at the SIFMA Basel III Endgame Roundtable. Q&A is expected.

- 10:00 AM Existing home sales, March (GS +0.7%, consensus -4.5%, last +9.5%)

- 11:00 AM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will participate in a moderated fireside chat on the economic outlook in Fort Lauderdale, Florida. Q&A is expected. On April 12th, President Bostic noted that his outlook for 2024 was “one cut toward the end of the year.” He said he expected inflation would “continue to fall, but much slower than I think many would like.”

- 05:45 PM Atlanta Fed President Bostic (FOMC voter) speaks: Atlanta Fed President Raphael Bostic will take part in a moderated fireside chat on the economic outlook in Coral Gables, Florida. Q&A is expected.

Friday, April 19

- There are no major economic data releases scheduled.

- 10:30 AM Chicago Fed President Goolsbee (FOMC non-voter) speaks: Chicago Fed President Austan Goolsbee will participate in a moderated Q&A at the Society for Advancing Business Editing and Writing’s 2024 annual conference in Chicago. On April 12th, President Goolsbee noted that there had been multiple CPI inflation readings “that were higher than we wanted,” but that PCE was “the better measure.” He noted that “if PCE is reinflating—we will stabilize prices.” President Goolsbee said that “the most important number to be watching on the inflation front here in the immediate term is what is happening with housing,” noting that “if that doesn’t go down to something like it was pre-COVID we will have a hard time getting the overall back to target.”

Source: DB, Goldman, BofA